Newsroom

Investment Talks - Italian politics take centre stage

London, UK, August 23, 2019

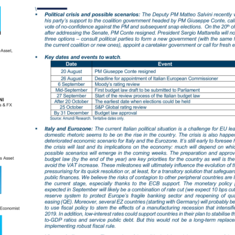

- Political crisis and possible scenarios: The Deputy PM Matteo Salvini recently withdrew his party’s support to the coalition government headed by PM Giuseppe Conte, calling for a vote of no-confidence against the PM and subsequent snap elections. On the 20th of August, after addressing the Senate, PM Conte resigned. President Sergio Mattarella will now weigh three options – consult political parties to form a new government (with the same forces of the current coalition or new ones), appoint a caretaker government or call for fresh elections.

- Italy and Eurozone: The current Italian political situation is a challenge for EU leaders, as domestic rhetoric seems to be on the rise in the country. The crisis is also happening in a deteriorated economic scenario for Italy and the Eurozone. It’s still early to foresee how long the crisis will last and its implications on the economy: much will depend on which of the possible scenarios will emerge in the coming weeks. The preparation and approval of the budget law (by the end of the year) are key priorities for the country as well is the need to avoid the VAT increase. These milestones will ultimately influence the evolution of the crisis, pressurising for its quick resolution or, at least, for a transitory solution that safeguards Italian public finances. We believe the risks of contagion to other peripheral countries are limited at the current stage, especially thanks to the ECB support. The monetary policy package expected in September will likely be a combination of rate cut (we expect 10 bps cut), a tired reserve system to protect Europe’s fragile banking sector and reopening of quantitative easing (QE). Moreover, several EZ countries (starting with Germany) will probably be “forced” to use fiscal policy to stem the effects of a manufacturing recession that intensified in H1 2019. In addition, low-interest rates could support countries in their plan to stabilise their debt-to-GDP ratios and service public debt. But this would not be a long-term replacement for implementing robust fiscal rule.

- View on Italian assets: The opening of the political crisis and the emergence of the resultant risk premium is quite evident. From a risk adjusted return perspective, BTPs could fare better than equities if the political crisis deepens or is prolonged to 2020. In fact, given the recent generalized fall in bond yields across the board, we believe the hunt for yield will keep investors’ interest in Italian bonds. Our analysis shows that the value of the Italian BTPs makes for half of the value of the remaining positive yield assets in the EUR denominated IG fixed income space, while representing just 12% of overall outstanding debt. Despite recent volatility, we expect that investors’ demand will remain very high, limiting the upside pressure on bond yields in the short term.

About Amundi

About Amundi

Amundi, the leading European asset manager, ranking among the top 10 global players[1], offers its 100 million clients - retail, institutional and corporate - a complete range of savings and investment solutions in active and passive management, in traditional or real assets. This offering is enhanced with IT tools and services to cover the entire savings value chain. A subsidiary of the Crédit Agricole group and listed on the stock exchange, Amundi currently manages more than €2.3 trillion of assets[2].

With its six international investment hubs[3], financial and extra-financial research capabilities and long-standing commitment to responsible investment, Amundi is a key player in the asset management landscape.

Amundi clients benefit from the expertise and advice of 5,600 employees in 35 countries.

Amundi, a trusted partner, working every day in the interest of its clients and society

Footnotes

- ^ [1] Source: IPE "Top 500 Asset Managers" published in June 2024 based on assets under management as of 31/12/2023

- ^ [2] Amundi data as at 31/03/2025

- ^ [3] Paris, London, Dublin, Milan, Tokyo and San Antonio (via our strategic partnership with Victory Capital)

Footnotes