Newsroom

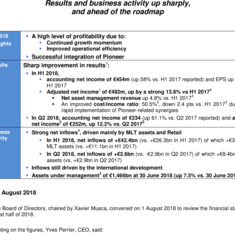

Results and business activity up sharply,

and ahead of the roadmap

|

H1 2018 Highlights |

|

|

Results |

Sharp improvement in results[1]:

|

|

Business activity |

|

London, 2 August 2018

Amundi’s Board of Directors, chaired by Xavier Musca, convened on 1 August 2018 to review the financial statements for the first half of 2018.

Commenting on the figures, Yves Perrier, CEO, said:

“In the first half of 2018, Amundi came in ahead of its strategic roadmap for both business activity and profitability. The integration of Pioneer has been successfully developed and is bearing fruit. These excellent results, in a less favourable environment, confirm the strength and the resilience of the Group's business model, which relies on its diverse business lines (client segments, investment expertise and regions). Amundi has a significant growth potential, based on strengthened investment expertise and a powerful international network”.

I. Sharp improvement in results

Amundi’s results rose substantially in both H1 2018 and Q2 2018 due to scissors effect of the increase in asset management revenues and the reduction in operating expenses.

These strong results confirm the Group’s ability to grow while keeping costs under control, in particular due to synergies related to the integration of Pioneer.

Accounting net income Adjusted[5] net income at comparable scope[6]

In the first half of 2018

Accounting income in H1 2018 (including integration costs and the amortisation of distribution contracts) amounted to €454m, up by a sharp 58% compared with H1 2017 reported, benefiting from the contribution of Pioneer (consolidated as from 1 July 2017), growth momentum and strong cost controls.

EPS reached €2.25, up 43.6% vs. H1 2017, compared with an accretion target of 30%, stated at the signing[7] of the Pioneer acquisition.

Adjusted data5

Net asset management revenue grew steadily (€1,347m, up 4.8%[8]), thanks to:

- Net management fees at €1,259m (up 3.5%8), in line with the growth in assets under management over 12 months; margins[9] proved resilient: average margin of 18.9bp vs. 19.3bp in H1 2017.

- A high level of performance fees (€88m, up 26.8%8), reflecting the funds’ strong performances[10] over the last 12 months.

The negative contribution of net financial income (-€7m) was linked mainly to interest expense and to the mark-to-market effect on the investment portfolio. Financial income in H1 2017 included an exceptional amount of investment capital gains realised in the context of the financing of the Pioneer acquisition.

Operating expenses fell sharply (€677m, down 4.6%8), due to the rapid execution of the Pioneer integration plan (approximately 70% of the workforce reductions had been completed at end-June 2018), despite the absorption of external research costs related to MiFID (Markets in Financial Instruments Directive).

The cost/income ratio therefore stood at 50.5% (among the lowest in the industry), a 2.4 point8 decrease from H1 2017, and gross operating income reached €664m, up 5.2%8 vs. H1 2017.

Taking into consideration the 63% increase in the contribution from equity-accounted entities (primarily the Asian joint ventures) and a lower tax charge of €188m, due mainly to the elimination of the dividend tax in France and the tax reform in the United States, adjusted net income, Group share totalled €492m, up 13.6%8 compared with H1 2017. This increase was higher than the stated target of 7% per year[11].

In the second quarter of 2018

Accounting income in Q2 2018 (including integration costs and the amortisation of distribution contracts) amounted to €234m, a sharp 61.1% increase vs. Q2 2017 reported.

Adjusted data[12]

Net asset management revenue increased by 2.8%[13]to €679m, due mainly to a 4.1%8 rise in net management fees.

Thanks to the decline in operating expenses (€340m, down 4.0%), the cost/income ratio stood at 50.2%, a 1.3 point decrease13 vs. Q2 2017. Gross operating income reached €337m, up 1.0%13 vs. Q2 2017.

Taking into consideration the improved contribution from equity-accounted entities (primarily the Asian joint ventures) and a sharply lower tax charge of €93m, adjusted net income, Group share totalled €252m, up 12.2%13 compared with Q2 2017.

II. A high level of activity in H1 2018

Net inflows were strong in H1 2018 +(€42bn, for an average target of €50bn per year), driven by medium/long-term assets, Retail and International.

After an exceptionally high first quarter, inflows in the second quarter were also solid (+€2.6bn vs. -€2.9bn in Q2 2017), as the continued inflows in medium/long-term assets offset the seasonal treasury product outflows.

In H1 2018

Amundi's assets under management amounted to €1,466bn at 30 June 2018, reflecting strong business activity (net inflows of +€42.4bn in H1 2018), with a slightly negative market effect (-€2.1bn).

Note: all variation figures below are computed vs a combined H1 2017 (6 months Amundi + 6 months Pioneer).

- The Retail segment enjoyed strong momentum in H1 2018, with net inflows of +€34.6bn (versus +€22.2bn in H1 2017), generated by all distribution channels. The French networks continued to deliver a strong commercial performance (+€3.2bn), driven by unit-linked life in insurance policy subscriptions (confirming the recovery observed since mid-2016). Flows remained brisk in the international networks, at +€5.0bn, reflecting the success of the partnership with UniCredit (in Italy in particular, with net inflows of +€4.4bn, mostly in MLT products, and driven by segregated accounts and unit-linked). Inflows for third-party distributors were +€3.0bn, driven by France and Asia. Flows were strong once again in the Asian joint ventures (+€23.5bn), primarily in China.

- Business activity in the Institutional segment was satisfactory at +€7.8bn in H1 2018 (compared with +€4.1bn in H1 2017), with robust commercial activity for sovereign and other institutional clients. Business activity in the Corporates & Employee Savings segment (-€10.7bn) was affected by seasonality in treasury products (‑€13.7bn), which was offset by strong inflows in MLT assets (+€3.0bn, in particular in Employee Savings).

By asset class, net inflows consisted primarily of MLT assets (+€36.5bn or 86% of the total), mainly in Multi-asset and Equities.

Commercial successes in H1 2018 included:

- Continued market share gains in ETFs: ETF inflows remained steady in H1 2018 at +€2.9bn[14] (Amundi is #3 in net flows within European ETF providers[15]), bringing assets under management to €40.5bn14 at 30 June 2018 in Europe (ranked #5 in AuM within European ETF providers15). Overall, passive management and smart beta assets under management amounted to €97bn14 at 30 June 2018, up 21% over 12 months.

- Ongoing development of real assets: Real estate recorded net inflows of +€1.3bn14 in H1 2018, bringing AuM to €29bn14 at 30 June 2018. Private debt increased with net inflows of +€1.1bn14 in H1 2018, bringing AuM to €6.8bn14 at 30 June 2018.

From a geographic viewpoint, net inflows continued to be driven by the International development with a significant contribution from Asia (+€30.1bn), led by the JVs, but also by Japan, Hong Kong and Taiwan, and from Italy (+€6.7bn, an increase over H1 2017) where the partnership with UniCredit is yielding results. In France, business activity was strong in MLT assets (Retail and Employee Savings Plans), offset by treasury product outflows.

Over one year, international assets under management increased by 14.6%, and they now represent 43% of Amundi’s total AuM, and 58% of AuM excluding Crédit Agricole and Société Générale insurance companies mandates.

In the second quarter of 2018

In Q2 2018, net inflows reached +€2.6bn, above the Q2 2017 level (-€2.9bn). The performance varied by client segment:

- In Retail, net inflows remained strong (+€12.9bn), due to momentum in the partner networks (+€2.7bn) and in all of the Asian JVs (+€11.4bn). The French networks (net inflows entirely in MLT assets at +€0.6bn vs. ‑€0.2bn in Q2 2017) and the Italian networks (+€1.7bn) benefited in particular from the appeal of segregated accounts and unit-linked. There were moderate net outflows of -€1.2bn for third-party distributors in a less favourable market environment which led to higher risk aversion in Europe.

- There were net outflows for the Institutional segment (-€10.3bn), related to seasonal outflows in treasury products used by Corporates (in particular to pay dividends), after very strong net inflows in Q1 2018. Business activity in Q2 for the other client segments was strong, driven mainly by Employee Savings Plans and by Institutional and Sovereign clients.

III. Other information

A solid financial structure

At 30 June 2018, Amundi's tangible equity totalled €1.9bn, stable relative to 31 December 2017, as capital generated from net income for the period (+€454m) was offset by the 2017 fiscal year dividend payment (-€504m).

In June 2018, rating agency Fitch confirmed Amundi’s A+ rating, the best in the sector.

Results of the capital increase reserved for employees

The subscription period for the capital increase reserved for employees (announced in February) was closed on 9 July. This operation, meant to strengthen employees’ sense of belonging following the Pioneer acquisition, was carried out in the context of existing legal powers as approved by the General Shareholders’ Meeting of May 2017.

Nearly 1,000 employees in 14 countries participated in this capital increase by subscribing 193,792 new shares (0.1% of the share capital) for a total amount of €10m. This operation did not have a significant impact on earnings per share.

Following this transaction, employees hold 0.3% of the share capital compared with 0.2% previously.

A notice regarding the admission of the new shares (ISIN code: FR0004125920) will be published by Euronext Paris on 2 August 2018. These new shares will be admitted to trading on the morning of 6 August. This issue brings the number of shares making up Amundi's share capital to 201,704,354 on 2 August 2018.

Financial disclosure schedule

- 26 October 2018: Publication of results for the first nine months of 2018

- 13 February 2019: Publication of full-year 2018 results

***

Amundi’s financial information for the first half of 2018 consist of this press release

and the attached presentation, which are available at http://legroupe.amundi.com

***

Footnotes

- ^ [1] All net income figures provided in this press release are net income, Group share.

- ^ [2] Adjusted data in H1 2018: before amortisation of distribution contracts (€25m after tax) and before costs associated with the integration of Pioneer (€12m after tax). In Q2 2018: before amortisation of distribution contracts (€12m after tax) and before costs associated with the integration of Pioneer (€6m after tax). Refer to methodology section on page 8 of this release.

- ^ [3] Change using comparable (6 months Amundi + 6 months Pioneer, or 3 months Amundi + 3 months Pioneer) and adjusted data

- ^ [4] Assets under management and inflows include assets under advisory and assets sold and take into account 100% of assets under management and inflows on the Asian JVs. For Wafa in Morocco, assets are reported on a proportional consolidation basis.

- ^ [5] Adjusted data in H1 2018: before amortisation of distribution contracts (€25m after tax) and before costs associated with the integration of Pioneer (€12m after tax). In Q2 2018: before amortisation of distribution contracts (€12m after tax) and before costs associated with the integration of Pioneer (€6m after tax). Refer to methodology section on page 8 of this release.

- ^ [6] Constant scope in 2017 and 2018: 6 months Amundi + 6 months Pioneer and 3 months Amundi + 3 months

- ^ [7] Amundi press release of 12/12/2016

- ^ [8] Change using combined and adjusted 2017 data

- ^ [9] Excluding performance fees

- ^ [10] Performance fees are recognised on the funds’ anniversary date, reflecting the performance over the previous 12 months.

- ^ [11] Target calculated based on 2017 adjusted and combined net income excluding the non-recurring level of financial income. Press release of 09/02/2018

- ^ [12] Adjusted data in H1 2018: before amortisation of distribution contracts (€25m after tax) and before costs associated with the integration of Pioneer (€12m after tax). In Q2 2018: before amortisation of distribution contracts (€12m after tax) and before costs associated with the integration of Pioneer (€6m after tax). Refer to methodology section on page 8 of this release.

- ^ [13] Change using combined and adjusted 2017 data

- ^ [14] Ex JVs

- ^ [15] Source: DB ETF Monthly Review & Outlook, end-June 2018

|

€m |

H1 2018 |

H1 2017 |

Change |

Q2 2018 |

Q2 2017 |

Change |

||||||

|

Adjusted net revenues 2 |

1,340 |

1,340 |

= |

677 |

688 |

-1.5% |

||||||

|

o/w Net management fees |

|

1,259 |

|

1,216 |

|

+3.5% |

|

643 |

|

618 |

|

+4.1% |

|

o/w Performance fees |

|

88 |

|

69 |

|

+26.8% |

|

36 |

|

43 |

|

-16.0% |

|

o/w Financial income and other net income 2 |

|

-6 |

|

55 |

|

NS |

|

-2 |

|

28 |

|

NS |

|

Adjusted operating expenses 3 |

-677 |

-709 |

-4.6% |

-340 |

-354 |

-4.0% |

||||||

|

Adjusted gross operating income 2 3 |

664 |

631 |

+5.2% |

337 |

334 |

+1.0% |

||||||

|

Adjusted cost/income ratio 2-3 |

|

50.5% |

|

52.9% |

|

-2.4 pts |

|

50.2% |

|

51.5% |

|

-1.3 pt |

|

Cost of risk & Other |

|

-10 |

|

-6 |

|

NS |

|

-6 |

|

-2 |

|

NS |

|

Equity-accounted entities |

|

25 |

|

16 |

|

+62.5% |

|

14 |

|

8 |

|

+70.3% |

|

Adjusted income before taxes 2-3 |

679 |

640 |

+6.1% |

345 |

339 |

+1.6% |

||||||

|

Taxes 2-3 |

-188 |

-208 |

-9.6% |

-93 |

-115 |

-19.3% |

||||||

|

Adjusted net income, Group share 2-3 |

492 |

433 |

+13.6% |

252 |

224 |

+12.2% |

||||||

|

Amortisation of distribution contracts after tax |

-25 |

-6 |

NS |

-12 |

-3 |

NS |

||||||

|

Pioneer integration costs after tax |

-12 |

-21 |

NS |

-6 |

-17 |

NS |

||||||

|

Net income, Group share |

454 |

406 |

+11.8% |

234 |

204 |

+14.3% |

1- Combined data in H1 2018 and H1 2017 (6 months Amundi + 6 months Pioneer) and in Q2 2018 and Q2 2017 (3 months Amundi + 3 months Pioneer).

2- Excluding amortisation of UniCredit, SG, and Bawag distribution contracts.

3- Excluding costs associated with the integration of Pioneer.

|

|

(€bn) |

AuM |

Net inflows |

Market effect |

Scope effect |

||

|

Amundi |

At 31/12/2016 |

1,083 |

|

|

|

||

|

|

Flows in Q1 2017 |

+32.5 |

+12.5 |

/ |

|||

|

|

At 31/03/2017 |

1,128 |

|

|

|

||

|

|

Flows in Q2 2017 |

|

-3.7 |

-3.1 |

/ |

||

|

|

At 30/06/2017 |

1,121 |

|

|

|

||

|

|

Integration of Pioneer |

/ |

/ |

/ |

+242.9 |

||

|

Amundi + Pioneer |

Flows in Q3 2017 |

|

+31.2 |

+5.3 |

/ |

||

|

|

At 30/09/2017 |

1,400 |

|

|

|

||

|

|

Flows in Q4 2017 |

|

+13.1 |

+12.7 |

/ |

||

|

|

At 31/12/2017 |

1,426 |

|

|

|

||

|

|

Flows in Q1 2018 |

|

+39.8 |

-13.5 |

/ |

||

|

|

At 31/03/2018 |

1,452 |

|

|

|

||

|

|

Flows in Q2 2018 |

|

+2.6 |

+11.4 |

/ |

||

|

|

At 30/06/2018 |

1,466 |

|

|

|

||

|

|

AuM |

AuM |

% chg. vs. |

Inflows |

Inflows |

Inflows |

Inflows |

Inflows |

||||

|

(€bn) |

30/06/2018 |

30/06/2017 |

30/06/2017 |

Q2 2018 |

Q1 2018 |

Q2 2017 |

H1 2018 |

H1 2017 |

||||

|

French networks1 |

110 |

103 |

+6.5% |

+0.6 |

+2.6 |

-0.2 |

+3.2 |

+1.1 |

||||

|

International networks |

122 |

113 |

+8.0% |

+2.1 |

+2.9 |

+4.1 |

+5.0 |

+5.2 |

||||

|

JVs |

140 |

105 |

+33.1% |

+11.4 |

+12.1 |

-0.8 |

+23.5 |

+7.3 |

||||

|

Third-party distributors |

182 |

169 |

+7.4% |

-1.2 |

+4.1 |

+5.7 |

+3.0 |

+8.5 |

||||

|

Retail |

554 |

490 |

+12.9% |

+12.9 |

+21.7 |

+8.8 |

+34.6 |

+22.2 |

||||

|

Institutionals2 and sovereigns |

375 |

344 |

+8.8% |

+6.1 |

+14.4 |

-2.9 |

+20.5 |

+4.8 |

||||

|

Corporates |

58 |

60 |

-2.0% |

-15.5 |

+2.2 |

-12.6 |

-13.2 |

-5.1 |

||||

|

Employee Savings Plans |

59 |

55 |

+6.3% |

+2.6 |

-0.1 |

+2.2 |

+2.5 |

+1.7 |

||||

|

CA & SG insurers |

421 |

414 |

+1.6% |

-3.6 |

+1.5 |

+1.6 |

-2.0 |

+2.7 |

||||

|

Institutionals |

913 |

874 |

+4.5% |

-10.3 |

+18.1 |

-11.7 |

+7.8 |

+4.1 |

||||

|

TOTAL |

1,466 |

1,364 |

+7.5% |

+2.6 |

+39.8 |

-2.9 |

+42.4 |

+26.3 |

1 French networks: net inflows on medium/long-term assets +€2.2bn in H1 2018 (+€0.6bn in Q2 2018)

2 Including funds of funds

|

AuM |

AuM |

% chg. vs. |

Inflows |

Inflows |

Inflows |

Inflows |

Inflows |

|||||

|

(€bn) |

30/06/2018 |

30/06/2017 |

30/06/2017 |

Q2 2018 |

Q1 2018 |

Q2 2017 |

H1 2018 |

H1 2017 |

||||

|

Equities |

244 |

213 |

+14.1% |

+2.4 |

+8.9 |

+2.8 |

+11.3 |

+4.1 |

||||

|

Multi-asset |

267 |

242 |

+10.2% |

+9.3 |

+5.8 |

+2.9 |

+15.1 |

+8.3 |

||||

|

Bonds |

657 |

638 |

+3.0% |

-3.6 |

+13.3 |

-3.7 |

+9.7 |

-3.0 |

||||

|

Real, alt. and structured assets |

71 |

67 |

+5.7% |

+0.4 |

+0.1 |

+0.8 |

+0.5 |

+1.7 |

||||

|

MLT assets |

1,238 |

1,160 |

+6.7% |

+8.4 |

+28.1 |

+2.9 |

+36.5 |

+11.1 |

||||

|

Treasury products |

228 |

204 |

+12.2% |

-5.7 |

+11.7 |

-5.7 |

+5.9 |

+15.2 |

||||

|

TOTAL |

1,466 |

1,364 |

+7.5% |

+2.6 |

+39.8 |

-2.9 |

+42.4 |

+26.3 |

|

|

AuM |

AuM |

% chg. vs. |

Inflows |

Inflows |

Inflows |

Inflows |

Inflows |

||||

|

(€bn) |

30/06/2018 |

30/06/2017 |

30/06/2017 |

Q2 2018 |

Q1 2018 |

Q2 2017 |

H1 2018 |

H1 2017 |

||||

|

France |

843* |

820 |

+2.8% |

-13.7 |

+14.3 |

-11.4 |

+0.6 |

+8.4 |

||||

|

Italy |

178 |

167 |

+7.0% |

+2.5 |

+4.1 |

+3.6 |

+6.7 |

+4.3 |

||||

|

Europe excl. France and Italy |

151 |

137 |

+10.1% |

-0.6 |

+2.5 |

+4.2 |

+1.9 |

+3.4 |

||||

|

Asia |

206 |

159 |

+30.2% |

+15.3 |

+14.8 |

-0.3 |

+30.1 |

+8.1 |

||||

|

Rest of world** |

88 |

82 |

+7.6% |

-0.8 |

+4.0 |

+1.0 |

+3.2 |

+2.1 |

||||

|

TOTAL |

1,466 |

1,364 |

+7.5% |

+2.6 |

+39.8 |

-2.9 |

+42.4 |

+26.3 |

||||

|

TOTAL excl. FRANCE |

624 |

544 |

+14.6% |

+16.4 |

+25.4 |

+8.5 |

+41.8 |

+17.9 |

* of which €406bn for CA & SG insurers

** Mainly US

-

-

H1 2018 Income statement

-

-

Accounting data

In H1 2018, the data corresponds to six months of activity for Amundi and six months of Pioneer's activity. This H1 2018 is compared with a reported H1 2017 that included only six months for Amundi.

-

Adjusted data

To present an income statement that is closer to the economic reality, the following adjustments have been made:

- In H1 2018: restatement of Pioneer-related integration costs and amortisation of distribution contracts (deducted from net revenues) with SG, BAWAG and UniCredit.

- In H1 2017: restatement of Pioneer-related integration costs and amortisation of distribution contracts (deducted from net revenues) with SG and BAWAG only (as the contract with UniCredit did not start until Q3 2017).

-

Combined data

The combined data are different from the pro forma data (as presented in the 2017 Registration Document), which included restatements for the financing assumptions for the acquisition of Pioneer: additional financing costs, reduced financial income.

Costs associated with the integration of Pioneer Investments:

- H1 2018: €18m before tax and €12m after tax

- H1 2017: €32m before tax and €21m after tax

Amortisation of distribution contracts:

- H1 2018: €36m before tax and €25m after tax

- H1 2017: €8m before tax and €6m after tax

-

-

Reminder of amortisation of distribution contracts with UniCredit

-

When Pioneer was acquired, 10-year distribution contracts were entered into with UniCredit networks in Italy, Germany, Austria, and the Czech Republic; the gross valuation (at acquisition date) of these contracts came to €546m (posted to the balance sheet under Intangible Assets). At the same time, a Deferred Tax Liability of €161m was recognised. Thus the net amount is €385m which is amortised using the straight-line method over 10 years, as from 1 July 2017.

In the Group's income statement, the net tax impact of this amortisation is €38m over a full year (or €55m before tax), posted under "Other revenues," and will be added to existing amortisations of the SG and Bawag distribution contracts of €11m after tax over a full year (€17m before tax).

-

-

Alternative Performance Indicators[1]

-

To present an income statement that is closer to the economic reality, Amundi publishes adjusted data which are defined as follows: they have excluded costs associated with the integration of Pioneer and amortisation of the distribution contracts with SG, Bawag and UniCredit since 1 July 2017 (see above).

To assess the new group’s performance on a comparable basis, Amundi also publishes combined data for H1 2017, which include six months of Pioneer and six months of Amundi. These combined and adjusted data are reconciled with accounting data as follows:

Footnotes

About Amundi

Amundi is Europe’s largest asset manager by assets under management and ranks in the top 10[1] globally. It manages more than 1.460 trillion[2] euros of assets across six main investment hubs[3]. Amundi offers its clients in Europe, Asia-Pacific, the Middle-East and the Americas a wealth of market expertise and a full range of capabilities across the active, passive and real assets investment universes. Headquartered in Paris, and listed since November 2015, Amundi is the 1st asset manager in Europe by market capitalization[4].

Leveraging the benefits of its increased scope and size, Amundi has the ability to offer new and enhanced services and tools to its clients. Thanks to its unique research capabilities and the skills of more than 4 500 team members and market experts based in 37 countries, Amundi provides retail, institutional and corporate clients with innovative investment strategies and solutions tailored to their needs, targeted outcomes and risk profiles.

Amundi. Confidence must be earned.

Visit amundi.com for more information or to find an Amundi office near you.

Follow us on

DISCLAIMER:

This document may contain projections concerning Amundi's financial situation and results. The figures given do not constitute a “forecast” as defined in Article 2.10 of Commission Regulation (EC) No. 809/2004 of 29 April 2004.

This information is based on scenarios that employ a number of economic assumptions in a given competitive and regulatory context. As such, the projections and results indicated may not necessarily come to pass due to unforeseeable circumstances. The reader should take all of these uncertainties and risks into consideration before forming their own opinion.

The figures presented were prepared in accordance with IFRS guidelines. Limited review procedures are underway for the condensed interim financial statements.

The information contained in this document, to the extent that it relates to parties other than Amundi or comes from external sources, has not been independently verified, and no representation or warranty has been expressed as to, nor should any reliance be placed on, the fairness, accuracy, correctness or completeness of the information or opinions contained herein. Neither Amundi nor its representatives can be held liable for any negligence or loss that may result from the use of this document or its contents, or anything related to them, or any document or information to which the document may refer.

Footnotes

17 Amundi figures as of June 30, 2018

Linked Topic

United Kingdom, April 27, 2018

Amundi - 1st quarter 2018 results

A strong start to the year, confirming Amundi’s growth trend Net inflows(1)of €40b

About Amundi

About Amundi

Amundi, the leading European asset manager, ranking among the top 10 global players[1], offers its 100 million clients - retail, institutional and corporate - a complete range of savings and investment solutions in active and passive management, in traditional or real assets. This offering is enhanced with IT tools and services to cover the entire savings value chain. A subsidiary of the Crédit Agricole group and listed on the stock exchange, Amundi currently manages more than €2.3 trillion of assets[2].

With its six international investment hubs[3], financial and extra-financial research capabilities and long-standing commitment to responsible investment, Amundi is a key player in the asset management landscape.

Amundi clients benefit from the expertise and advice of 5,600 employees in 35 countries.

Amundi, a trusted partner, working every day in the interest of its clients and society

Footnotes

- ^ [1] Source: IPE "Top 500 Asset Managers" published in June 2024 based on assets under management as of 31/12/2023

- ^ [2] Amundi data as at 31/03/2025

- ^ [3] Paris, London, Dublin, Milan, Tokyo and San Antonio (via our strategic partnership with Victory Capital)

Footnotes